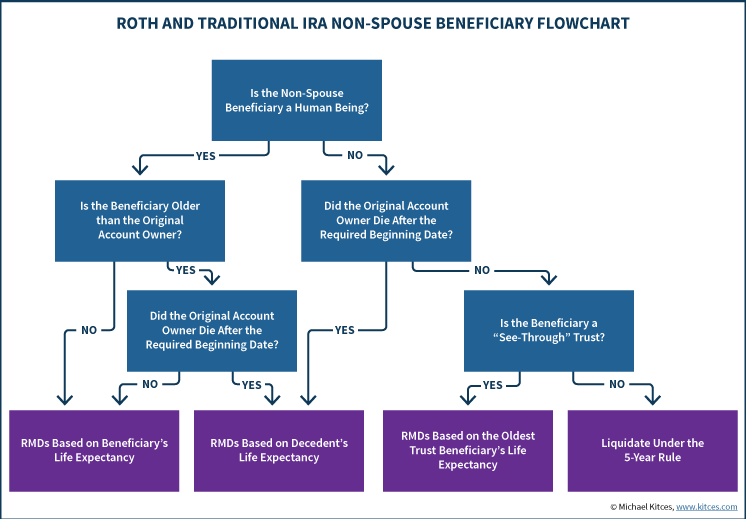

Ira Distribution To Beneficiaries Tax Consequences

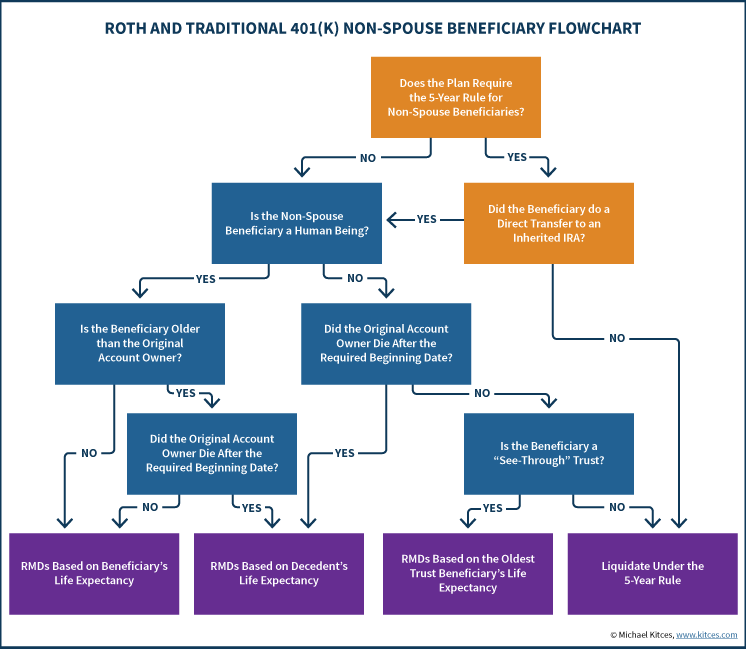

Non Spouse Beneficiaries Rules For An Inherited 401k

:max_bytes(150000):strip_icc()/RothIRAwithdrawalconsequences-5c4a16cd46e0fb0001b8c43b.jpg)

Roth Ira Withdrawals Read This First

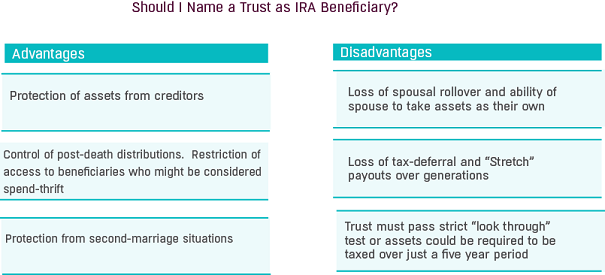

Naming Your Trust As Beneficiary Of An Ira Windgate Wealth Management

How The Secure Act Impacts Retirement Planning Retirement Field Guide

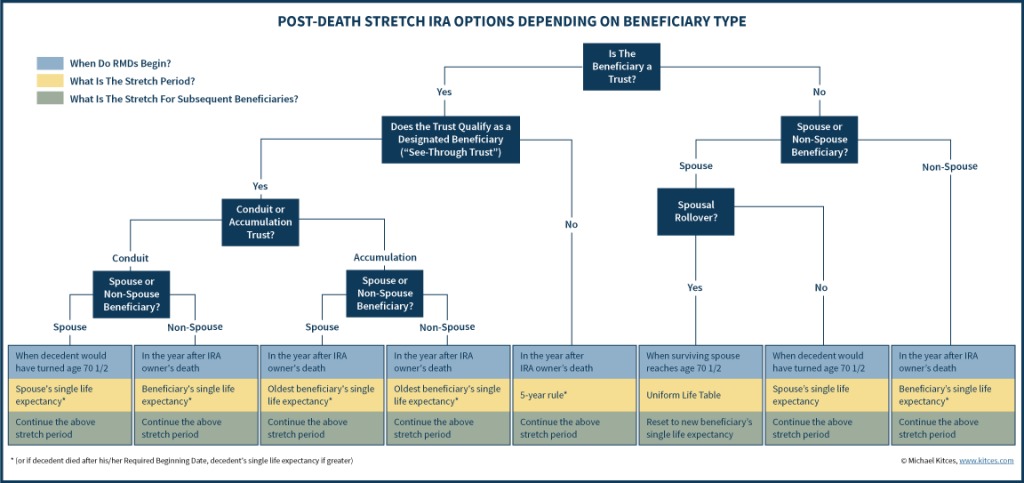

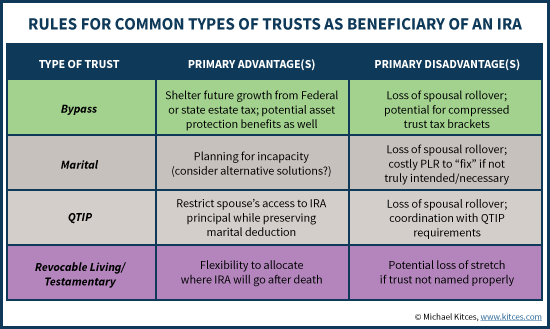

Getting Stretch Ira Treatment With An A B Trust

Non Spouse Beneficiaries Rules For An Inherited 401k

Ira distributions are considered income and as such.

Ira distribution to beneficiaries tax consequences. Whether you withdraw money for yourself or distribute your balance to a trust or trust beneficiaries the internal revenue. Similar to traditional ira rules the lump sum option does not require you to set up a separate account. A stretch ira is an estate planning strategy that extends the tax deferred status of an inherited ira when it is passed to a non spouse beneficiary. You may designate your own ira beneficiary.

If the owner was your spouse you re in a different position than any other beneficiary. The tax consequences of an inherited individual retirement account depend on your relationship to the late account owner. If it is due the holder s death then the 10 distribution penalty does not apply. Estate tax consequences for non spouse beneficiaries.

Beneficiaries of a roth ira may receive all assets in the roth bda ira at once. For non spouses the way you decide to receive these funds determines the taxes due. That means that tax is paid when the holder of an ira account or the beneficiary takes distributions in the case of an inherited ira account. Most ira distributions are taxable as ordinary income.

Roth iras also allow for tax free and penalty free withdrawals as long as the account is at least five years old and the original owner is at least 59 5. Generally the entire interest in a roth ira must be distributed by the end of the fifth calendar year after the year of the owner s death unless the interest is payable to a designated beneficiary over the life or life expectancy of the designated. The deceased owner s estate will owe estate taxes if the total value of all her assets combined with the value of the ira or 401 k exceeds. If you are under 59 you ll be subject to the same distribution rules as if the ira had been yours originally so you cannot take distributions without paying the 10 early withdrawal penalty unless you meet one of the irs penalty exceptions.

Ira assets can continue growing tax deferred. The entire fair market value of the ira or 401 k will be included in the value of the deceased owner s estate for estate tax purposes if the account is left to anyone other than a surviving spouse.

Taxing Consequences What To Do With A Large Ira That Has Been Inherited Or Accumulated Wiseradvisor Com

Getting Stretch Ira Treatment With An A B Trust

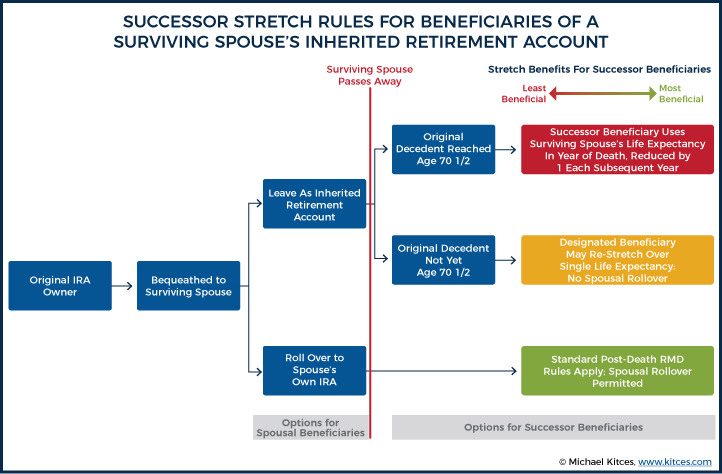

Spousal Rollover Rules For Inherited Roth Traditional Iras

Publication 590 B 2019 Distributions From Individual Retirement Arrangements Iras Internal Revenue Service

Look Before You Leap Into A 529 Plan Journal Of Accountancy

Ira Beneficiary Checklist For Send To Your Cpa Network Hard Copies Customized Glossy Card Stock Appleby S Ira Publications

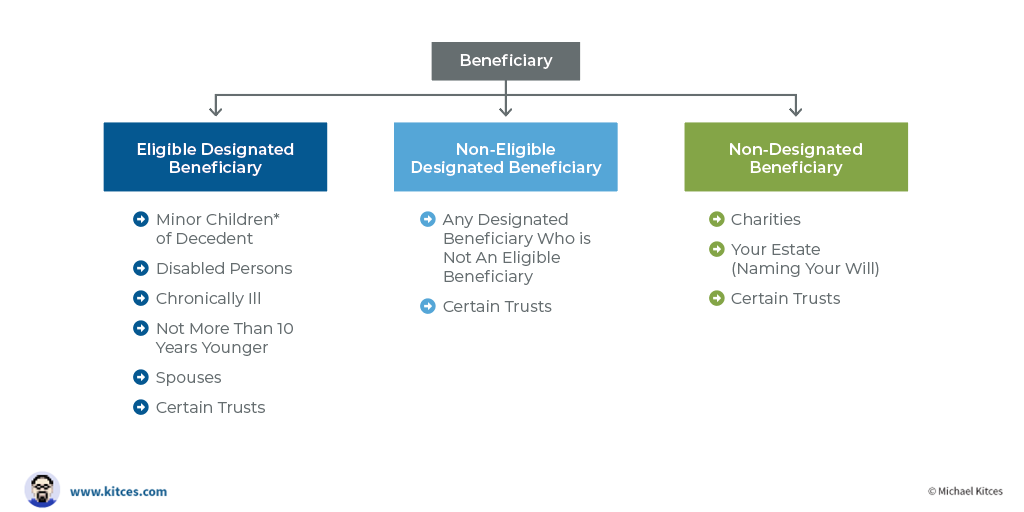

New Secure Act Stretch Ira Rules For Eligible Designated Beneficiaries

/RothIRAwithdrawalconsequences-5c4a16cd46e0fb0001b8c43b.jpg)

Roth Ira Withdrawals Read This First

Rmds And The Cares Act A Boon For Retirement Planners Financial Planning

Understanding The Ira Mandatory Withdrawal Rules Marketwatch

Have You Inherited An Ira It S Time To Compare Your Options

New Cares Act Would Bring Tax Relief For Retirement Accounts Financial Planning

New Stretch Ira Rules Could Make This Type Of Trust More Popular

:max_bytes(150000):strip_icc():saturation(0.2):brightness(10):contrast(5)/GettyImages-1353850562-5a09f8cd494ec9003739b86b.jpg)